The BrewDog Lesson: How to Build Brand Equity That Survives the Shelf

Alessandro Camaioni and James Cahill weigh in on the strategic move

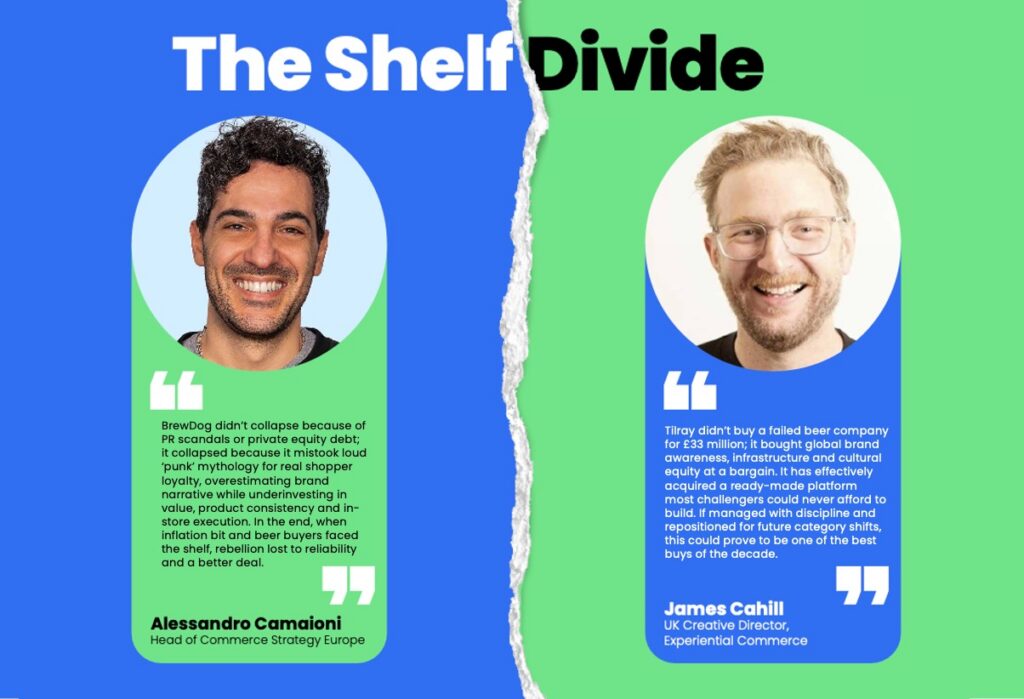

The announcement has been made, and industry professionals are already sharing their perspectives: BrewDog, once valued at an eye-watering £2 billion, has been swallowed by a cannabis and drinks conglomerate, Tilray Brands, for £33 million.

Industry professionals are pointing the finger towards former CEO James Watt’s hubris and the cascading toxic workplace scandals; financial press highlights the suffocating weight of private equity debt. Meanwhile, the rest of the internet is most likely debating the morality of a company that built itself on “Equity for Punks,” only to wipe out the investments of 200,000 everyday advocates (some of them giving thousands of £££ to the once growing business), basically overnight.

BrewDog’s craft beer revolution went flat (Photo Credit: The Telegraph)

But if we look past all that, we can see that BrewDog didn’t suddenly die this week; it has been slowly bleeding out at the shelf edge for years. This is the ultimate cautionary tale of what happens when a brand mistakes a marketing mechanic (the crowdfunding, the loud, disruptive PR stunts) for fundamental shopper loyalty.

If we were to overlay the BrewDog collapse with our latest Momentum Global Shopper Study (November 2025), the data would reveal a company that was fundamentally out of step with how modern consumers actually browse, buy and, ultimately, drink.

For a decade, BrewDog convinced the industry that a loud origin story would be enough to insulate a premium price point almost indefinitely. That their drinkers weren’t just shoppers, but a ‘community.’ Mythology marketing at its finest. We all fell for it—marketers more than anyone else. But our proprietary data dismantles this illusion. When we asked shoppers what actually drives their long-term brand loyalty, “values alignment, community and origin stories” mattered to a mere 15% of respondents. The actual drivers? “Consistently good products” (42%) and “rewards, discounts and value” (37%).

BrewDog built a multi-billion valuation by over-indexing entirely on that 15%, assuming their ‘punk’ narrative would give them a free pass on the relentless dynamics of CPG. But as inflation skyrocketed and the cost-of-living crisis bit hard, shoppers stood in the supermarket beer aisle, looked at a four-pack of Punk IPA and asked a ruthless question: Where is the actual value here? The answer was nowhere. Product innovation had stalled, replaced by gimmicky limited editions, while the rebellion narrative had grown exhausted and hypocritical. Shoppers realized they weren’t paying a premium to fund a movement; they were just overpaying for an average pale ale.

This leads directly to their second strategic mistake: BrewDog misunderstood the fundamental dynamics of the category they were trying to conquer. Our research highlights a fascinating divide in how shoppers treat ‘new’ vs. ‘legacy’ brands. In fast-moving, low-risk categories like packaged snacks, new entrants and disruptive challengers tend to outpace legacy brands (40% vs 31% preference). But in alcoholic beverages, data shows how established players still lead significantly; in beer, specifically, shoppers will experiment occasionally, but their default behavior is anchored in reliability and trust.

BrewDog mistakenly believed they could operate with the volatile energy of a disruptive snack brand forever. But once you scale to a £2bn valuation and secure distribution in every major multiple in the country, you are no longer a rebel, you are the establishment. And in the establishment, you need to compete on supply chain efficiency, operational excellence and legacy trust, precisely the attributes BrewDog had spent years actively battling against.

BrewDog’s recent Barbecue campaign (Photo Credit: Kévin Houdmon and Julien Dussier)

This way, they got stuck in the middle: an overpriced supermarket staple relying on a rebellion that ended years ago. And because they thought they were still fighting a craft –beer culture war, they brought a PR knife to a trade marketing gunfight. They operated under the assumption that loud stunts, CEO-written manifestos and ‘punk’ packaging generated enough upper-funnel brand gravity to pull shoppers down the aisle. Meanwhile, established players like Heineken (Beavertown) and AB InBev (Camden) have demonstrated that success in the beer aisle comes from disciplined, strategic and consistent in-store execution.

Our research proves just how critical this physical battleground remains. Over 48% of our respondents actively notice in-store retail media, but, more crucially, a staggering 79% are likely to consider a new brand based on in-store branded displays and 68% are swayed by promotional pricing.

And this is where BrewDog lost. While ‘big beer’ dominated retail media networks, secured prime gondola ends and executed aggressive, margin-tight promotional pricing strategies (on platforms like Clubcard and Nectar) that spoke directly to the 56% of shoppers who cite “rising prices” as their primary worry, BrewDog relied on brand equity built predominantly in the early 2010s. We now know that ‘punk’ loses to a better deal every single time.

We specialise in Experiential Commerce: the purchase moment is not just a transactional endpoint, but a powerful brand-building opportunity in itself—one where upper-funnel experiences seamlessly find their way into lower-funnel environments.

BrewDog negates this philosophy. Over the years, particularly at the beginning, they built an incredibly loud brand that commanded global attention. They capitalized that equity by opening a network of premium outlets. But time and time again, they fundamentally failed to orchestrate the final moment of truth, treating the physical shelf as a passive endpoint rather than an active battleground. They assumed the brand work was done before the shopper entered the store. How wrong.

Tilray has bought a globally recognised logo for pennies, but they have inherited a monumental challenge. BrewDog’s collapse is a stark reminder to every brand that commerce cannot be an afterthought in today’s landscape. You can generate millions in earned media, but if your fundamental shopper marketing equation (value, reliability, in-store execution) doesn’t add up, consumers will simply pick something else.

The punks didn’t sell out. They were just out-shopped.

But what if £33 Million isn’t a Collapse… it’s a reset—and possibly the steal of the decade.

You framed BrewDog’s £33 million sale to Tilray Brands as a humiliation—a £2 billion rocket ship reduced to the price of a London townhouse. But valuation is not value. And in this case, I think Tilray may have just bought a global brand platform at a staggering discount.

I think you can argue that what’s actually being acquired here isn’t a distressed beer business. It’s unaided awareness, global distribution, an owned retail footprint, brewing infrastructure and, crucially, cultural memory. (brand salience?)

Because, let’s be honest, brands don’t disappear because their multiples contract.

BrewDog still has name recognition most challenger breweries would spend decades and nine-figure budgets trying to build. It has bars in major cities. It has established listings in supermarkets. It has international reach. You can’t replicate that from scratch for £33 million—not even close.

From Tilray’s perspective, this is portfolio arbitrage.

Tilray isn’t just a cannabis company dabbling in drinks; it has been building a beverage strategy for years, assembling craft assets and distribution capabilities across North America and Europe. What it lacked was a globally recognisable masterbrand with attitude. BrewDog brings that instantly.

And timing matters.

Beer volumes are under pressure. Premiumisation has stalled. Consumers are price sensitive. That’s exactly when you buy—not when growth curves look perfect. Tilray isn’t paying for BrewDog at its peak mythology valuation; it’s buying during reputational fatigue and operational strain. Turnarounds are made in moments like this.

There’s also a category adjacency play that commentators are underestimating.

As regulations evolve around cannabis-infused beverages in various markets, owning brewing infrastructure, flavor expertise and established retail relationships becomes strategically powerful. BrewDog’s rebellious DNA—which, as you rightly argue, could be seen as exhausted—could also translate seamlessly into next-generation functional or infused drinks if managed correctly. Under new ownership, that narrative can be rewritten.

And let’s be honest: much of BrewDog’s valuation collapse reflects capital structure and governance turbulence, not consumer abandonment at scale. The core product still sells. The brand still moves volume. It simply wasn’t optimized for its cost base.

For £33 million, I don’t actually think that Tilray bought a sinking ship. Sure, it bought a ship with dents, a global flag and a loyal (and possibly quieter) crew.

If managed with operational discipline, sharper pricing architecture and refreshed innovation, this won’t be remembered as the day BrewDog fell. It could be remembered as the day someone recognized that distressed assets with enduring awareness are the best bargains in business.

Written by Alessandro Camaioni, Head of Commerce Strategy, Europe and James Cahill, UK Creative Director, Experiential Commerce at Momentum Worldwide